In this article

A quarter of directors surveyed in Diligent’s What Directors Think 2025 report said improving cybersecurity and risk management was a top priority. Much of those improvements come down to internal controls, which have long been essential to risk assessment and management. However, isn’t always easy to incorporate internal controls into business processes. The COSO Internal Control Framework gives organizations a strategic path forward.

This framework helps businesses embed internal controls and internal controls management software in their day-to-day activities. When used effectively, it assures shareholders and the board that the organization meets ethical and security standards.

Organizations that do adopt the COSO Internal Control Framework can also be more efficient, more secure, and, ultimately, more resilient as the risk landscape evolves. Here, we’ll explain:

The COSO Framework helps organizations connect their internal controls to their business process. It reaches back to 1992 when the Committee of Sponsoring Organizations (COSO) met to create a more significant relationship between the risk and business landscapes. Several private sector organizations also contributed to the framework, including:

In 2013, they updated the COSO Framework to include a diagram of the relationship between all elements of internal controls. They edited it again in 2017 with the enterprise risk management framework, demonstrating how to prioritize risk and establish a connection between risk and business performance.

According to the COSO definition, internal control is a process designed to provide reasonable assurance with regard to achieving operations, reporting and compliance objectives. Boards of directors, management and other relevant personnel, should oversee this process on an ongoing basis.

Streamline processes, automate workflows and provide meaningful insights to leadership. Enhance compliance and risk management with this essential checklist.

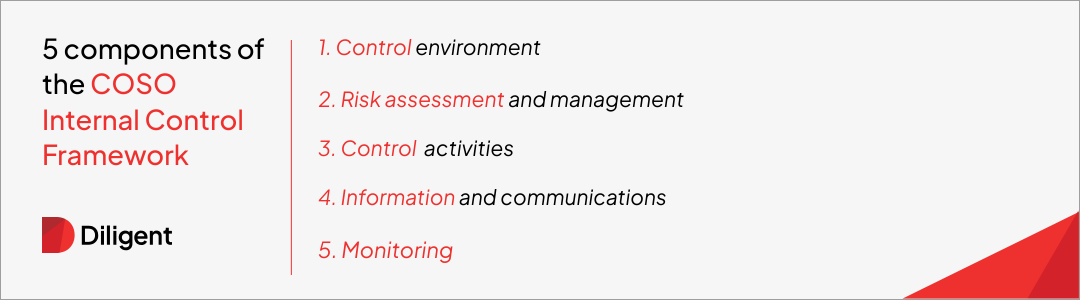

The five components of the COSO Framework establish the key areas where organizations need to work towards compliance.

The five components are:

In the control environment, organizations should verify that their business processes meet industry risk standards by testing all controls. This ensures that all activities are done responsibly, reducing an organization’s legal liability. Organizations should also work to meet all regulatory compliance requirements.

Risks are inevitable. That doesn’t mean organizations should ignore them. Businesses can minimize the possible harm by assessing the risks their organization currently faces and putting a plan in place to manage and mitigate them. This process should be ongoing or even automated so that organizations can identify new risks as they emerge.

Control activities are integral to risk management, ensuring that all business activities tie back to internal controls. Those controls should both support business performance and reduce the organization’s risk exposure.

An organization’s communications also need to follow strict requirements. Various legal, ethical and industry standards apply to internal and external communications. Privacy policies and other application controls are examples of how organizations can apply controls to communication processes.

Risks can evolve, as do organizations’ systems, software and processes. Monitoring ensures that these changes don’t expose the organization to risk. An internal auditor is usually responsible for this, but external auditors often monitor organizations in relation to regulatory compliance. Both auditors will ultimately report to the board of directors.

Nested within each of the above components are principles that explain the controls in greater detail. These are:

The COSO Framework establishes how the organization will complete all business processes. This embeds risk management into all parts of the organization, facilitating legal and regulatory compliance. Once all controls are in place, the framework also prioritizes monitoring, which helps organizations verify that all internal controls are followed and that they can stay ahead of emerging risks.

Learn to articulate the true ROI of safer systems.

While the COSO Framework does create a strategic path forward for risk management, it also has its limitations that organizations should be aware of.

These are three key benefits organizations can expect by following the COSO Internal Control Framework:

As effective as the COSO Framework can be, it can also be restricting in the following ways:

The COSO Internal Control Framework is widely used, but it’s one of many that organizations today rely on to strengthen controls and manage risk. There is overlap between frameworks, but there are also key distinctions:

Here’s how these frameworks compare at a glance:

Putting the COSO Internal Control Framework into practice helps organizations strengthen governance, improve risk management and ensure operational and financial integrity. Below is a simplified roadmap for adopting COSO’s components and principles:

Implementing the COSO framework — or any new internal control or risk management system — can uncover obstacles that hinder your progress. However, even if your resources are limited, you’re unsure about roles and responsibilities or facing another complication, you can still adopt strong controls. Below are proven strategies to help you navigate key challenges:

Risk, compliance, and audit teams may have a vision for using the COSO internal control framework before leadership fully understands and is ready to sign off.

Solutions: Engage executive leadership early. Articulate how internal controls support strategic goals, regulatory requirements and reputation risk. Use real-world examples like those below to show failures or successes in your industry, helping illustrate what’s at stake.

Teams may begin to develop internal controls based on their distinct needs, then fail to communicate with other teams, leading to a fragmented and duplicative internal control system.

Solutions: Form a cross-functional implementation team with representation from finance, compliance, operations, IT and HR. This helps ensure the internal control system will adapt to different use cases. Set up recurring check-ins throughout implementation to share updates and remove barriers.

Smaller organizations may not have the budget for dedicated internal compliance teams, but even larger enterprises may struggle to allocate enough time and staff to deploy a single internal controls framework across complex systems.

Solutions: Start with a risk-based, phased implementation approach, prioritizing high-risk areas first. Leverage existing processes where possible, and consider the right-sized tools rather than building everything from scratch or jumping into a tool too robust for your needs.

Internal controls are often shared across teams, creating confusion about who oversees the process, who executes it and who is responsible for maintaining it daily.

Solutions: Define and document responsibilities for each COSO component and principle. This will enable you to assign and hold specific team members accountable for specific parts of the framework. Responsible, Accountable, Consulted and Informed charts can clarify ownership.

Employees may be used to specific ways of working and struggle to adapt to the new internal controls.

Solutions: Rather than bolting on internal controls, consider how they can integrate into existing workflows or systems. Train staff on the “why” behind controls so they’re inspired to help implement them, not just the “what” and “how.”

Small businesses may struggle to find robust tools that suit their budgets, while larger enterprises often lack tools that can span entities and jurisdictions.

Solutions: Use existing data sources and automate controls where possible. Invest in scalable tools that support documentation, risk tracking and reporting to streamline your internal controls system.

The COSO internal control framework is flexible and scalable by design, making it well-suited to various industries. While the components remain the same, how organizations interpret, implement and prioritize them can vary based on their industry’s risks, regulations and operations.

Below are some key ways COSO can be applied and tailored across key sectors.

Organizations in the financial services industry face regulations like Basel III and SOX. Fraud risk is high, and internal audit integration is essential. Controls in this industry are often targeted toward high-volume, high-risk transactions.

Applying the COSO Framework to financial services includes an emphasis on a strong governance and control environment to withstand heavy regulations. Detailed risk assessments and robust monitoring systems are also critical to ensure the internal controls are effective and defensible. Financial services organizations may layer COSO with risk frameworks like COSO Enterprise Risk Management or the Federal Financial Institutions Examination Council (FFIEC) guidelines for additional protection.

Manufacturers often prioritize efficiency and supply chain integrity. Given their vast inventory and equipment, controls also emphasize asset protection. Environmental, health and safety compliance has also emerged in recent years.

As a result, the COSO control activities are typically physical, involving regular inventory counts and maintenance logs. Risk assessments may dig into logistics, production downtime or quality failures. Internal controls are in place, and manufacturers monitor plant-level performance indicators and safety inspections.

Information security and data privacy are critical in this industry. Most organizations will be subject to strict regulations like GDPR. Controls will also focus on protecting intellectual property, scaling growth and managing party and vendor risks.

Technology companies use IT internal controls heavily, aligning with COSO’s tech principles. Rapid change and innovation also require more continuous risk reassessment than other industries. Software companies should seek to cultivate a control environment that supports agile structures while maintaining accountability.

Like financial services, healthcare is a highly regulated industry. Many healthcare regulations, like HIPAA, focus on safeguarding patients’ personally identifiable information. Organizations in this industry must also emphasize clinical and billing accuracy, regulatory reporting and ethical practices.

Healthcare internal controls are rooted in cross-functional coordination involving clinical, administrative and financial teams. Monitoring often includes real-time data dashboards and audits, as healthcare organizations are frequent targets of cyberattacks. Fraud risk can also include internal abuse and external claims fraud, expanding the scope of internal controls.

COSO is designed to be scalable and tailored to fit organizations of all sizes. Whether you’re a small startup or a global enterprise, the COSO Framework helps improve internal controls, manage risk and build trust with stakeholders. The key is adapting the principles proportionally to your resources, complexity and objectives.

COSO provides structure without being prescriptive, making it ideal for SMBs to formalize processes without overcomplicating operations. Using the framework can help SMBs protect against fraud and theft, demonstrate transparency to lenders, investors and donors and support growth by systematizing operations.

However, SMBs’ focus will be slightly different than their larger counterparts:

Large organizations need a unified framework to manage complexity, cross-functional risk, and regulatory compliance. COSO provides a common language and structure across business units and geographies. Enterprises commonly use COSO to comply with SOX and financial reporting requirements, integrate controls with enterprise risk management (ERM) and unify global supply chain, data privacy and third-party risk controls.

With the essentials already covered, enterprises should use COSO to:

A Rome-based credit management company needed to set up its internal audit function. At that time, the board brought on a new Chief Controls Officer, who was charged with developing an internal controls system, enhancing audit committee activities, and providing ongoing guidance around risk. Like in many SMBs, the Chief Controls Officer had a small team that needed to have a significant impact.

The team first set up and implemented the Diligent One Platform to manage, track and monitor internal controls, which they developed based on the COSO Internal Control Framework. The platform streamlined every implementation step, from assessing risks to managing and monitoring controls to reporting on audits and risk posture.

Together, the new control system and the tools to execute it empowered the audit team to report on issues and provide evidence, which risk owners can update within the platform. They can also tie risk assessments directly to the owners so they can truly own and manage risk.

After rapid consolidation in the beverage industry, the company acquired at least 30 companies. This expansion increased business complexity and resulted in significant challenges for the audit team. The merging of multiple organizations had distinct data, requirements, and ways of working, including internal controls.

Adopting the Diligent One Platform enabled the company to supply one set of controls for all legal entities across the globe and audit those controls quickly and efficiently. The tool became the company’s “center of excellence” for control development and design. Using Diligent One, the audit team developed and refined 150 internal controls in just two years, providing a clear roadmap for how the business can operate efficiently, securely and compliantly.

Implementing the COSO framework is only the first step. Ongoing measurement and evaluation are essential to ensuring your internal controls do what they’re meant to: reduce risk, ensure compliance and support strategic objectives.

“Stakeholders now want everything in real-time. It used to be we could report things three months later. Now, three months is becoming three days,” says AIG Executive Vice President and Chief Auditor Naohiro Mouri.

You should measure internal controls' effectiveness by how well they are designed, implemented and functioning. Here are key questions to ask and steps to take to evaluate different aspects of your controls:

The COSO Internal Controls Framework provides a strong foundation for internal control and risk management. When paired with governance, risk and compliance (GRC) platforms and purpose-built AI, COSO becomes even more powerful, offering organizations a pathway to smarter, faster, more responsive controls.

GRC platforms unify risk, compliance and internal control management. While COSO offers the principles and structure, a GRC system is a vital tool for:

Process automation helps implement and maintain COSO-aligned controls with less manual effort. Emerging tools use AI to elevate internal control and risk management further, identifying patterns, predicting risks and automating decisions.

“With the right technology and automations, you can take an enterprise-type product, develop your audits and audit reporting in a way that’s streamlined and automated. It adds a ton of value to your process and to your organization,” says Cherry Hill Advisory Chief Executive Officer Mike Levy.

AI tools can:

The COSO Internal Control Framework provides valuable insight into how risk management should look. However, it doesn’t prescribe what an organization should do day-to-day to maintain that framework. The internal audit committee needs to operate on an always-on basis, but it can be challenging to prioritize risks, track remediations, and develop reports on risk and revenue opportunities.

Diligent’s Internal Audit Checklist equips teams with next-level efficiency and strategic insight to keep up with internal audit’s ever-expanding scope. Explore the five essential steps that help leading audit teams navigate growing responsibilities, COSO Internal Control Framework implementation and evolving regulations with confidence. Download the checklist to learn more.

COSO stands for the Committee of Sponsoring Organizations of the Treadway Commission. It is a joint initiative that developed a widely accepted framework for internal control, risk management and fraud deterrence. The COSO Framework helps organizations design, implement, and evaluate internal controls across operations, compliance and reporting.

The five components of the COSO Internal Control Framework are:

These components work together to promote effective internal control across the organization.

COSO itself is not legally mandated, but its use is strongly encouraged or indirectly required by several regulations. For example, under the Sarbanes-Oxley Act (SOX), U.S. public companies must establish internal controls over financial reporting, and the COSO Framework is the most commonly used standard to meet that requirement.

The COSO 2013 Framework updated the original 1992 version by:

While the core structure (the five components) stayed the same, COSO 2013 offers greater clarity, relevance and adaptability for today’s organizations.

The COSO Internal Control Framework is the most widely used standard for complying with Section 404 of the Sarbanes-Oxley Act (SOX), which requires public companies to establish and report on internal controls over financial reporting (ICFR).

COSO helps organizations:

Beyond SOX, COSO provides a flexible, scalable model used to comply with other regulations, including:

Yes. The COSO Framework is easily adaptable, making it suitable for organizations of all sizes and across sectors.

Resources and tools that can help with COSO implementation include:

Best practice recommends:

Controls should evolve with your organization’s risks and objectives to stay effective and compliant.